Trends & Tides – RBI Monetary Policy April 2026

The RBI’s Monetary Policy Committee (MPC) kept the repo rate and policy stance unchanged in its April 2026 meeting, amid risks to growth and inflation outlook. The MPC statement noted that the economy is facing a supply shock and that it is prudent to wait and watch the evolving growth-inflation outlook.

The MPC statement noted that the intensity and duration of the conflict in West Asia and the resultant damage to energy and other infrastructure pose risks to the economic outlook. The statement also highlighted that supply chain dislocations and the risk of second-round effects render the future inflation trajectory uncertain.

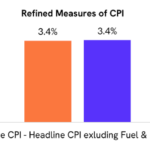

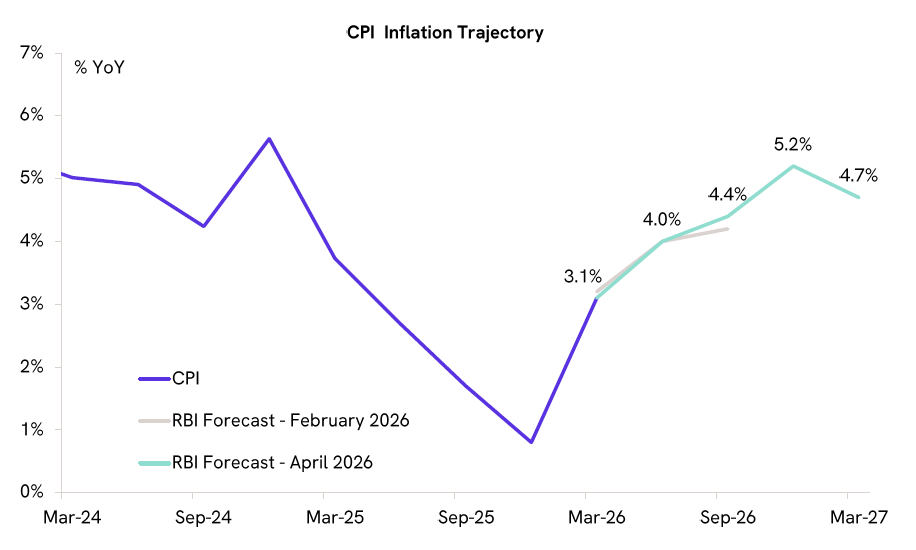

The RBI projected FY27 inflation at 4.6% YoY, with upside risks driven by energy price pressures and weather disturbances. The West Asia conflict has imparted significant uncertainty to the near-term inflation outlook. However, near-term food supply prospects have been bolstered by a robust rabi crop, offering some comfort.

The RBI projected FY27 real GDP at 6.9% YoY, assuming the adverse impact of the conflict remains contained. Elevated energy prices, coupled with supply shocks, would act as a drag on domestic production. Merchandise exports may also be impacted by disruptions to key shipping routes. Further escalation of the conflict and weather-related events pose downside risks to the domestic growth outlook.

The two-week ceasefire in West Asia has eased tensions for now, but there are still upside risks to inflation and downside risks to growth. Adding to the uncertainty are forecasts of a below-normal monsoon due to El Niño conditions, which could further weigh on agricultural output and price stability. Against this backdrop, we expect the RBI to maintain a prolonged pause.